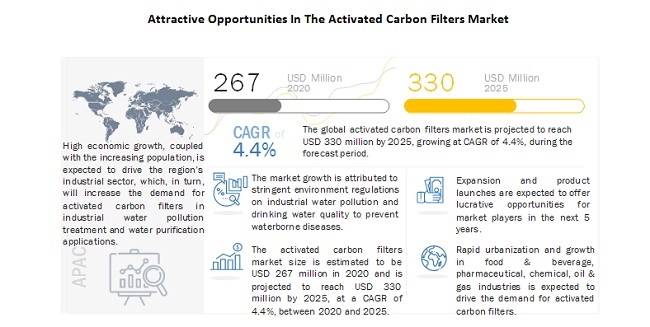

The global activated carbon filters market size is estimated at USD 267 Million in 2020 and is projected to reach USD 330 Million by 2025, at a CAGR of 4.4%, between 2020 and 2025. Activated carbon filters are used to remove organic compounds, and free chlorine from water to make it suitable for drinking and reuse in manufacturing processes or to discharge in water bodies. They are used to remove organic elements, such as humic acid and fulvic acid from potable water to prevent the formation of trihalomethanes, a class of carcinogens. They are also used for air/gas filtration in various industries. The filter media, which is used in the filtration process is activated carbon, also known as activated charcoal. Activated carbon is a form of carbon that removes organic compounds from liquids and gases by a process known as “adsorption”. It is extremely porous and thus has a very large surface area available for adsorption.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=213859954

The industrial water pollution treatment application is expected to be the largest, and drinking water purification application is expected to be the fastest-growing segment in the overall market. The global activated carbon filters market is mainly driven by the implementation of stringent regulations by regional governments and environmental agencies to control water pollution. Also, activated carbon filters are used to treat industrial discharge to re-use it in the manufacturing rocess again. Re-use of industrial discharge water and water pollution control are the two major making industrial water pollution treatment the largest application in the market.

APAC is the largest as well as the fastest-growing market for activated carbon filters market.

APAC is estimated to be the largest market for activated carbon filters in 2019. The market for this region is segmented into China, India, Japan, Malaysia, Indonesia, and the Rest of APAC. According to the World Bank, APAC is the fastest-growing region in terms of both population and economy. The region has witnessed significant growth in the past decade, accounting for over one-third of the world’s GDP. High economic growth, coupled with the increasing population, is expected to drive the region’s industrial sector. This is expected to increase the demand for activated carbon filters in water pollution treatment and water purification applications.

Recent Developments

- In January 2020, Kuraray expanded its Mississippi (US) activated carbon plant, which will increase the capacity of the plant by 50 million pounds of granular activated carbon (GAC) annually. GAC is used as filter media in activated carbon filters. This expansion will help the company to cater to the growing needs of activated carbon filters in the North American region.

- In April 2020, Cabot Corporation acquired Shenzhen Sanshun Nano New Materials Co., Ltd (SUSN) (China). This acquisition will help the company to strengthen its market position in the APAC region.

The key companies profiled in this report on the activated caron filters market include TIGG LLC (US), Puragen Activated Carbons (US), Cabot Corporation (US), Westech Engineering (US), Kuraray Co. Ltd. (Japan), Lenntech B.V. (The Netherlands), Donau Carbon Corporation (Germany), General Carbon Corporation (US), Sereco S.R.L. (Italy), Carbtrol Corp (US).

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=213859954